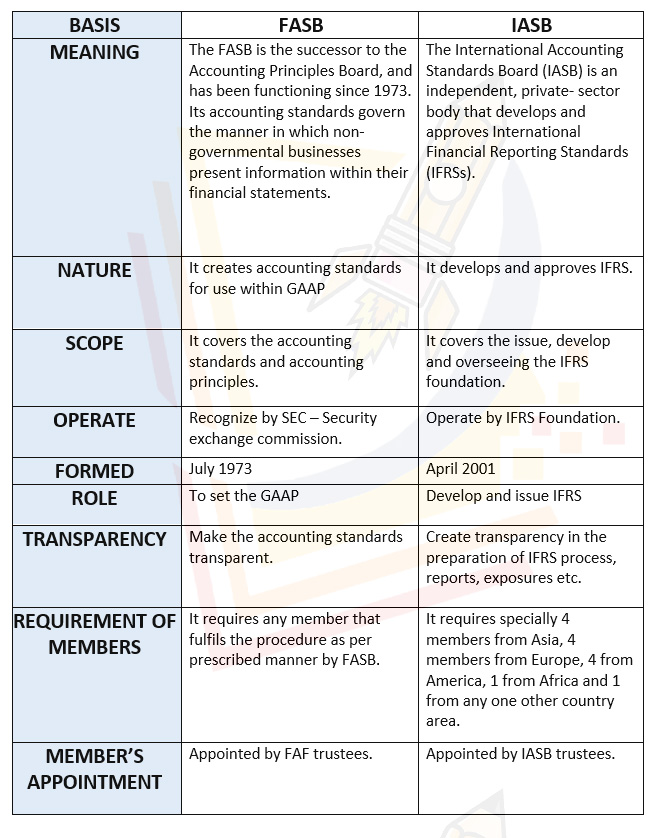

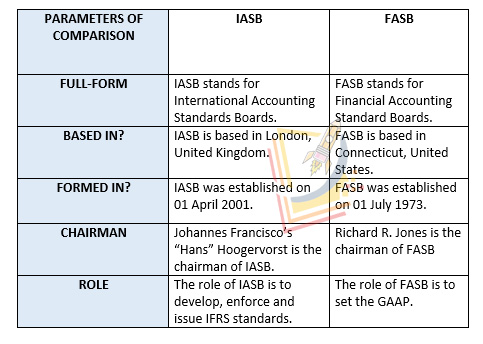

The International Accounting Standards Board (IASB) is an independent, private-sector body that develops and approves International Financial Reporting Standards (IFRSs).

The IASB operates under the oversight of the IFRS Foundation. The IASB was formed in 2001 to replace the International Accounting Standards Committee (IASC).

Currently, the IASB has 14 members.

THE IASB'S ROLE

Under the IFRS Foundation Constitution, the IASB has complete responsibility for all financial reporting-related technical matters of the IFRS Foundation including:

- full discretion in developing and pursuing its technical agenda, subject to certain consultation requirements with the Trustees and the public

- the preparation and issuing of IFRSs (other than Interpretations) and exposure drafts, following the due process stipulated in the Constitution

- the approval and issuing of Interpretations developed by the IFRS Interpretations Committee.

OVERVIEW:

- The IASB replaced the IASC Board of the International Accounting Standards Committee (IASC) with effect from this date. The IASC was formed in 1973.

- Until 31 March 2010, the IFRS Interpretations Committee was named the International Financial Reporting Interpretations Committee (IFRIC). IFRIC replaced the Standards Interpretations Committee (SIC) of the IASC with effect from 1 April 2001. The SIC was part of the original IASC structure formed in 1973.

- Until 31 March 2010, the IFRS Advisory Council was named the Standards Advisory Council (SAC).

- Formerly the Analyst Representative Group (ARG).

IASB BOARD REQUIREMENTS

COMPOSITION : Effective from 1 December 2016, IASB normally has 14 board members, of whom one is appointed as Chair and one as Vice-Chair. IASB members are appointed for an initial term of five years.

Terms are may be renewable once for a further term of three years, with the possibility of renewal up to a maximum of five years, in line with procedures developed by the Trustees for such renewals, however, the terms may not exceed 10 years in total length of service as a member of the Board.

The current size of the Board is a result of the 2015 Constitution review, which reduced the number from 16 to 14 members.

GEOGRAPHICAL BALANCE: To ensure a broad international diversity, the constitution requires four members from the Asia/Oceania region; four from Europe; four from the Americas; one from Africa; and one appointed from any area, subject to maintaining overall geographical balance.

BOARD MEMBER QUALIFICATIONS : The main qualification for membership is professional competence and practical experience.

The group is required to represent the best available combination of technical expertise and diversity of international business and market experience.

IN SUMMARY, The International Accounting Standards Board (IASB) is an independent body that sets accounting standards for businesses and organizations around the world with the goal of developing a single set of high-quality, understandable, and enforceable global accounting standards that can be used by all companies, regardless of their size or location. The IASB's standards are called International Financial Reporting Standards (IFRSs) which are used by more than 130 countries around the world.

COMPARISON TABLE BETWEEN THE INTERNATIONAL ACCOUNTING STANDARDS BOARD (IASB) AND THE FINANCIAL ACCOUNTING STANDARDS BOARD (FASB)

DIFFERENCE BETWEEN THE INTERNATIONAL ACCOUNTING STANDARDS BOARD (IASB) AND THE FINANCIAL ACCOUNTING STANDARDS BOARD (FASB)